Let’s be real about online sales…

You put a lot of hard work into building your store, perfecting your products, and attracting customers. Many people think that once a transaction passes, they sigh with relief. But the reality is different.

A ‘transaction success’ never marks a successful sale. You must maintain thorough customer service and clear communications to ensure the order's completion without going through disputes and chargebacks.

Disputed transactions drain your business finances. From delayed delivery to quality mismatches and hidden fees, these disputes can tarnish your reputation and increase churn rates.

So, to prevent disputes and welcome more successful sales, here’s a guide on the differences between transaction amount and disputed amount with examples and best practices.

Content Index

What Is Transaction Amount?

The transaction amount is the total amount paid for a purchase. For instance, if a customer pays ₹2,500 to purchase a pair of shoes online, the transaction amount is ₹2,500.

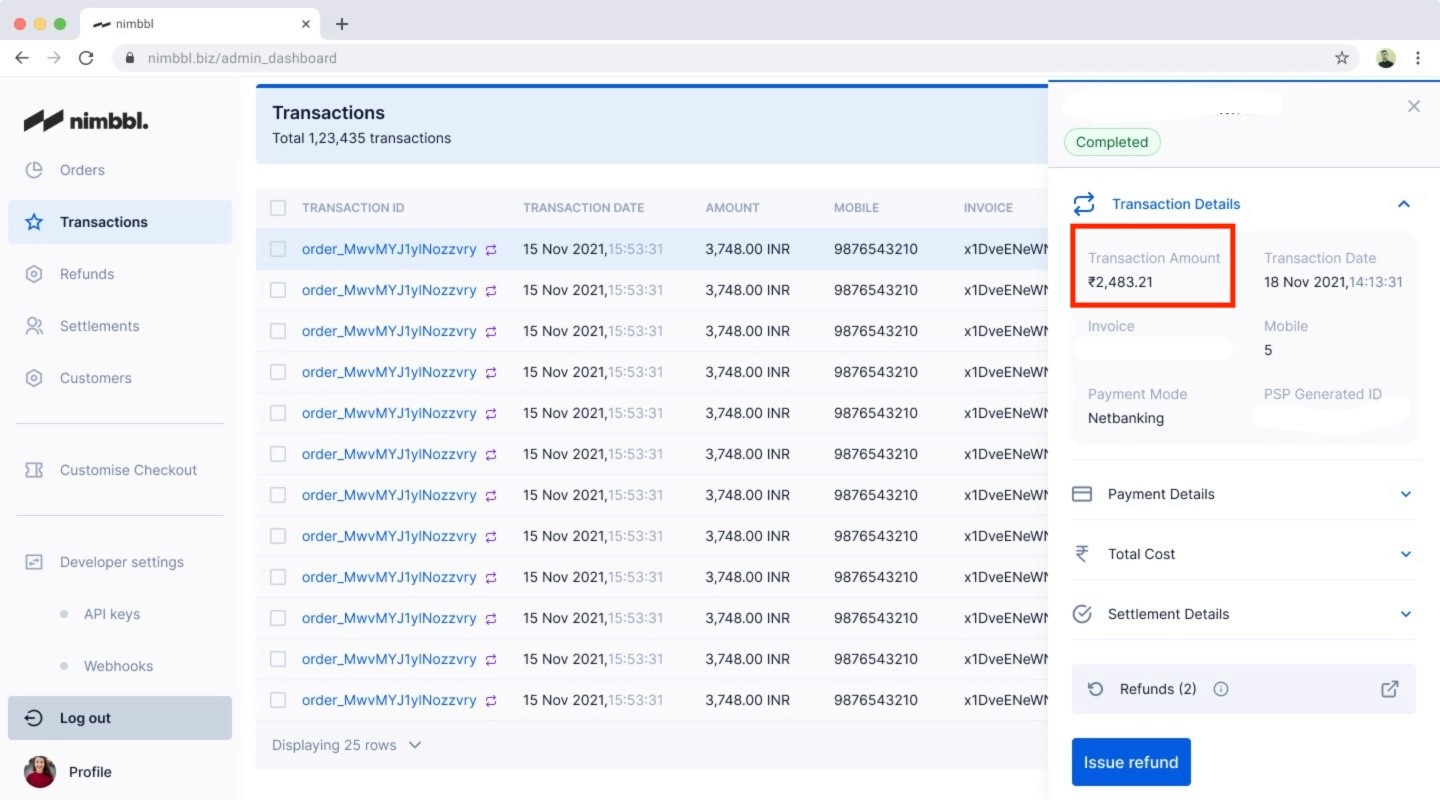

Similarly, the image below shows the Nimbbl transactions dashboard, where the transaction amount is ₹2,483.21.

Nimbbl transaction dashboard

What Is a Disputed Amount?

The disputed amount is the sum of money from a purchase or portion of a transaction that a customer contests with the seller in a dispute case.

Suppose a customer ordered groceries online with a total order value of ₹1,500, and they received an expired product worth ₹495. In this case, they can dispute the expired product and ask for a refund of the disputed amount ₹495. A few common reasons for disputes include faulty items, non-delivery, wrong product delivery, fraudulent payments, etc.

The Relationship Between Transaction and Disputed Amounts

The key difference between the transaction amount and the disputed amount is that while the transaction amount is the total order value, the disputed amount is the portion challenged by the customer.

According to the Digital Trust Index, as online sales continue to soar, so does the frequency of disputes and chargebacks. The data from Sift Global Network shows that the average dispute rate in Q3 of 2024 increased by 78% year-over-year. Overall, the global chargeback volumes are projected to reach 377 million transactions by 2026, a 42% increase from 2023.

Here’s how transactions lead to disputes in online sales.

Incorrect billing

This happens when a business charges the wrong amount to the customer. It can be mistakenly charging the same amount twice, a difference in actual and advertised charges, and hidden charges.

For instance, a customer subscribes to an online streaming service for Rs 5900 monthly. They agree to a monthly billing cycle and pay for the first month. After a few months, the customer decides they no longer wish to continue the service and attempts to cancel their subscription.

However, the company failed to process the cancellation properly and continued charging the customer for the next month, even though the customer was no longer using the service. The next billing cycle charges the customer Rs 5900 again without prior notice. When customers notice this charge on their bank statements, they contact the company for a refund and cancellation confirmation but do not receive a satisfactory response or resolution.

Frustrated, the customer files a chargeback with their credit card provider, stating that the charge was unauthorised and that the service was not canceled as requested.

Delivery issues

Delivery issues occur when customers pay for products or services but don't receive them as expected. This can include complete non-delivery of physical or digital products, partial delivery of ordered items, significant delays beyond promised delivery timeframes, or delivery to incorrect locations. These issues create a disconnect between what customers paid for and received, often leading to disputes.

For example, John buys an online e-book for Rs 2000 from a website. After purchase, he receives a confirmation email but no link to download the e-book. John tried connecting with the merchant but didn't get any response. After waiting for a week, he raised a dispute with his bank.

Authorisation issues

Transactions also lead to disputes due to unauthorised charges—the amount charged without the customer’s approval. For example, Mark books a hotel room online for Rs 5000. The hotel places a pre-authorization hold of Rs 7000 on his credit card for incidentals.

After his stay, he checked out of the hotel, and the final bill was only Rs 5000, but the Rs 7000 pre-authorization hold was never released. Mark contacts the hotel, requesting that the Rs 7000 hold be released. The hotel promises it will be refunded, but nothing happens. After waiting for weeks, Mark contacts his bank to raise the dispute.

Quality issues

Disputes over product quality arise when the product description or image online does not match the actual product. For example, a customer buys a ‘genuine’ leather briefcase at ₹4,999, but upon receipt, they find it’s synthetic leather. On raising this concern with the company, the customer didn’t receive a proper response. In this case, they can initiate a dispute for mentioning ‘genuine leather’ in the product description.

Importance of Monitoring Both Amounts

Dispute amounts can significantly impact the business’s cash flow by delaying fund collection. Customers and payment processors may hold off payment in case of multiple disputes, leading to uncollectible amounts and a direct hit on the cash flow. You cannot recognise revenue unless you resolve the conflict and settle the payment.

In online sales, dispute amounts like chargebacks and refunds impact the company’s cash flow by reducing the disputed amount from revenue. Refunds are better than chargebacks because chargebacks mitigate the sale amount and incur additional payment processing fees.

Besides financial implications, customer disputes can result in lower retention and higher reputational risk. So, to avoid frequent disputes, monitor both transaction and dispute amounts when they occur. It helps in:

Risk management: You can identify potential fraud, defective products, issues with pricing, product descriptions, or shipping policies. It also helps you spot iffy transaction patterns and proactively detect potential chargeback schemes.

Maintaining business health: Tracking the dispute rates and the dispute-to-transaction ratio helps improve operational efficiency. For instance, if you have high dispute rates in specific product categories, you can audit those to identify problem areas.

Similarly, if you see more disputes from first-time buyers than repeat ones, you can analyse the product descriptions, policy pages, and onboarding process to improve the process.

Legal and Regulatory Framework

As eCommerce has evolved, so has the Indian legal framework, which helps you handle transactions and disputes well. Here are the primary laws that govern Indian eCommerce:

The Information Technology (IT) Act, 2000

The IT Act mandates the protection of sensitive personal data, such as financial information like card numbers and CVVs. It deals with online transaction issues, digital signatures, and cybercrimes, outlining the legal provisions for electronic records security and setting standards for certifying digital signature authorities.

The Sales of Goods Act, 1930

The Sales of Goods Act regulates an entity's shipping policies and sales information. It provides standards as to what eCommerce companies should cover in their terms, guarantees, and transfer of ownership in commodities. Further, the act also mandates stating whether or not return/refund options are available.

Consumer Protection Act, 2019

The Consumer Protection Act protects consumer rights from unfair trade practices in online transactions. It provides an e-filing system to simplify dispute resolution and ensures faster redressal of consumer grievances. The Act also provides provisions for misleading ads and product liability and holds the service providers and manufacturers accountable for faulty goods.

Consumer Protection (E-commerce) Rules, 2020

In 2020, the government modified the Consumer Protection Act, adding rules for eCommerce entities to prevent consumer manipulation for unreasonable profits, unfair cancellation, and other deceptive trade practices. These rules mandate eCommerce companies to provide transparent information about their legal name, contact details, and address. They must also provide detailed product information, including pricing and country of origin.

Best Practices for Merchants To Avoid Chargebacks

While there’s no way to eliminate disputes and eCommerce fraud, you can prevent them and resolve online payment problems faster by implementing the following best practices:

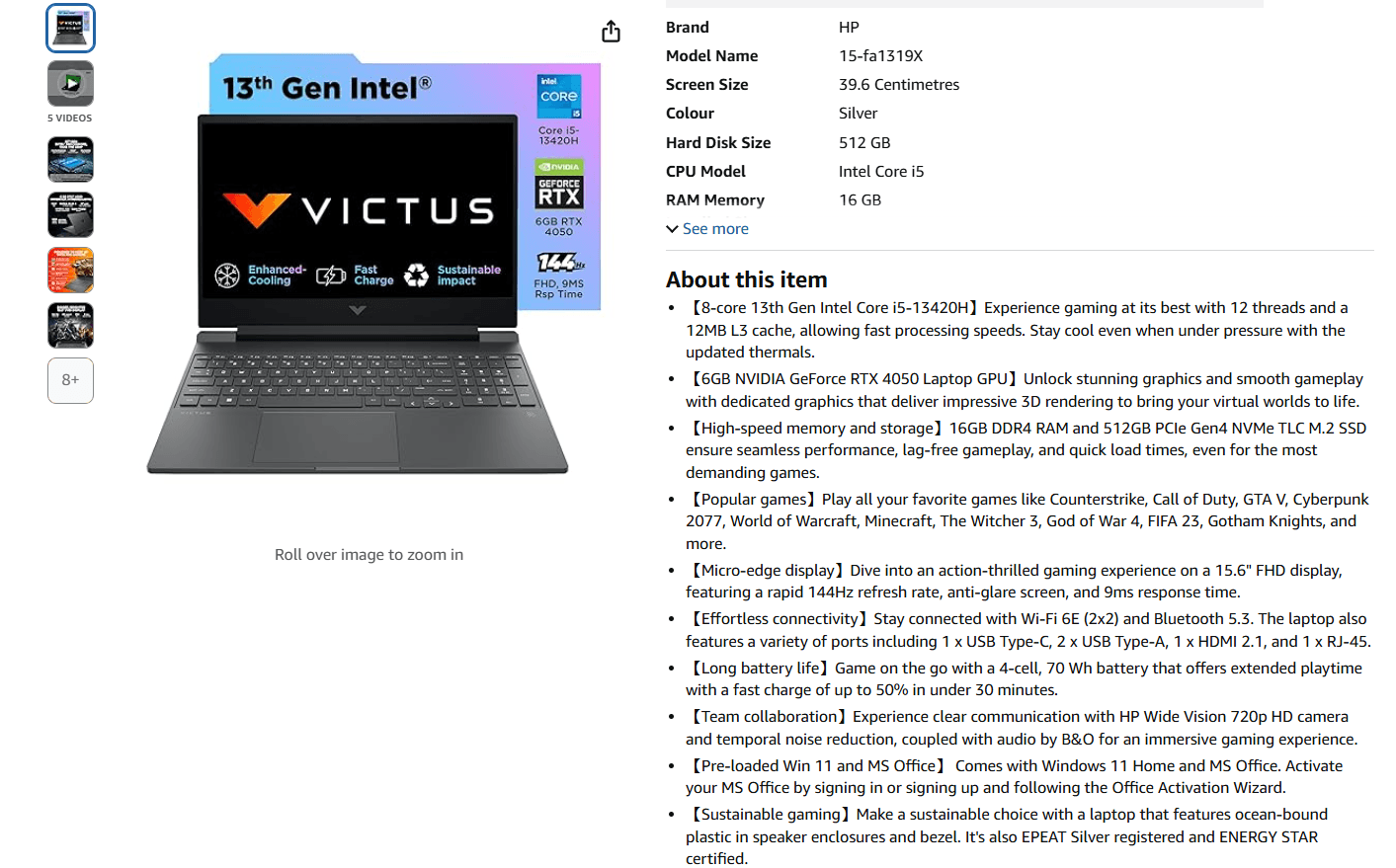

Show accurate product descriptions

Avoid using stock photos or misleading ads. Make sure your product descriptions and images represent the item you sell accurately. Here’s an Amazon product description for a laptop. It includes everything about the product, from brand to model name, product features, and 5 product videos.

Source: Amazon.in

Clarify return, refund, and cancellation policies

Mention each product's return/refund and cancellation policies at the time of sale. This might help prevent disputes and chargebacks for cancelled transactions. Also, include your terms and conditions near the payment button during checkout.

Confirm orders

Maintain clear customer communication through order and payment confirmations, dispatch, and delivery emails. Updating customers on each step of the process allows them to track their orders and helps prevent unnecessary disputes. Also, let customers know if a specific product is out of stock or will be delivered lately before they purchase.

Use tools to track transactions

Implementing the right tools to track transactions and disputed amounts can help you prevent and resolve disputes. Payment platforms like Nimbbl make tracking easy with all-in-one dashboards. You can track all your operations in one place and track transactions and refunds in real-time.

With multiple payment gateways, you can prevent delayed and cancelled transactions using Nimbbl. If customers face issues with one provider, they can switch over to another with minimal effort.

Case Studies

Here are a few examples of how merchants can deal with disputed amounts and chargebacks effectively.

Example 1

A customer orders a table for ₹400 but does not receive it within the promised timeframe. After several failed attempts to contact the merchant’s help desk, the customer disputed the order with her bank, demanding a chargeback.

Outcome: The bank reviewed the evidence and verified the customer’s claim. Consequently, they issued a chargeback, refunding the order amount to the customer and deducting it from the merchant.

Tip: You can prevent such cases of non-delivery and resultant chargeback by maintaining clear customer communications. You can extend the delivery date or inform customers about delayed delivery and stockouts before the customer places an order.

Example 2

A customer purchases a digital course for Rs 200000 from an online learning platform. The website states that the course is a one-time payment with lifetime access. After completing the course, the customer sees an unexpected recurring charge of Rs 10000 monthly for "premium content access," which they did not sign up for.

The customer contacts the merchant, but the support team is slow to respond. Frustrated, the customer files a chargeback with their bank, claiming they were charged for a service they did not authorise.

Why This Leads to Chargeback: The customer wasn’t aware of the recurring charges for "premium content access" because they weren’t clearly explained at the time of purchase. The terms and conditions around recurring payments were unclear, leading to confusion.

Tips: Use bold text or pop-up notifications to highlight any recurring payments. Customers should know exactly what they’re signing up for. Ensure that all fees, including subscription charges, are clearly explained before the customer completes the purchase.

Conclusion

While transaction amounts build up your revenue, disputed amounts can lead to chargebacks and financial losses. It can happen for various reasons like non-delivery, unauthorised transactions, fraud, incorrect billing, etc.

Putting in a little effort to monitor your transactions can go a long way in preventing disputes. Implementing a few best practices, like clear communication, sending transaction invoices, written authorisation, etc., can help reduce the odds of disputed transactions.

So, improve your policy and product pages and manage your transactions well. To simplify things, use tools like Nimbbl that centralise all transaction details to provide you with all the information at once.

Try Nimbbl today!

Merchant Dashboard