Imagine this: You run high-end electronic products from your website. One day, you suddenly notice a surge in the order volume of the most expensive items. However, your happiness turns into a scary experience the next day. You start receiving chargeback notifications and complaints related to unauthorised transactions.

Result? Loss of customers, loss of brand reputation, and loss of your hard-earned money.

If this has happened to you or you watched someone go through something similar, settle down. We have a lot to say.

Online payments are revolutionary. However, they are highly prone to security threats, and hackers are becoming more sophisticated at fraud tactics every day.

According to a recent Juniper study, online payment frauds caused $38 billion in merchant losses in 2023, predicted to increase to $91 billion in 2028.

One of the biggest threats to an online retailer is securing your online transactions and protecting your customers. In this blog post, we will discuss tips to increase online payment security for online businesses.

Content Index

Online Payment Security Issues eCommerce Merchants Must Know

How to Ensure Online Payment Security-Tips for eCommerce Merchants

What is Online Payment Security?

Online payment security is a practice and system that protects digital transactions from unauthorised access, data breaches, and fraud.

It is a combination of various practices, procedures, and technologies that ensure the authenticity of payment information. These measures also protect your company from legal disputes in case of fraud or data breach.

Glossary of complex terms used in this blog

PCI-DSS (Payment Card Industry Data Security Standard) is the set of security rules companies must follow to protect customer credit card information. |

Glossary

Types of Online Payment Security

Online payment security is of the following types:

Authentication

Authentication implements an additional layer of protection by asking users to provide another verification along with their password. This includes SFA (single-factor authentication), 2FA (Two-factor authentication), and MFA (Multi-factor authentication).

Card CVV verification, OTP, and biometrics are common authentication factors.

Data Encryption

Data encryption converts payment information into codes to prevent misuse for payment fraud.

Firewall and network security

Firewalls and network security protect payment infrastructure from hackers, malware, etc.

Fraud detection and prevention

Fraud detection and prevention monitor online transactions for malicious activities. It helps block/prevent fraudulent transactions using advanced ML algorithms.

Payment Card Industry Data Security Standard Compliance (PCI-DSS)

PCI-DSS is a security standard compliance that protects customer data used by companies. It aims to minimise the risk of data breaches.

Secure Payment Gateways

Payment gateways process credit card transactions and protect customer credit or debit cards from unauthorised access.

Security Updates and Patches

These include regularly updating and patching the security system to protect payment infrastructure. It helps secure customer data and critical systems from cyber-attacks and unauthorised access.

Tokenisation

Tokenisation replaces sensitive payment information with unique numbers known as tokens to process payments. It hides the original card details and processes the payment using the token.

Online Payment Security Issues eCommerce Merchants Must Know

Some of the biggest issues Indian eCommerce merchants face when accepting payments include:

Security threats and fraud

Security threats and fraud are consistent threats to online payment. Cybercriminals and hackers continuously develop new tactics to exploit the online payment system. These threats include identity theft, credit card theft, and phishing attacks.

These attacks result in significant financial losses and put businesses at risk of losing customer data. Repeated incidents of fraud erode customer trust, decreasing sales and customer loyalty.

Some of the standard methods of online security and payment system threats and frauds include:

Chargeback fraud or friendly fraud: This happens when the buyer makes a legitimate purchase and later disputes the charge with the bank. They claim they did not receive the product or did not authorise the payment at all. This results in the merchant losing the product and the payment.

Clean fraud: This involves using authentic information from a stolen card to make a purchase. Fraudsters use authentic but stolen data and credit card information to buy expensive items. These transactions blend in with legitimate transactions, making detection difficult.

Triangulation fraud: This involves customers making purchases with fake online vendors. These fake sellers use the customer transactions as a gateway to steal card details, either using them for further fraud or selling them to a third party.

According to PwC’s Global Economic Crime and Fraud Survey 2022, financial frauds on transactions made to or from platforms accounted for 89% of all platform frauds in India.

These include unauthorised digital purchases, triangulation, and identity theft.

How to Ensure Online Payment Security-Tips for eCommerce Merchants

With a few prevention tips, ECommerce stores can improve online payment security and systems. Here are a few tried and tested tips:

Know the basics of PCI-DSS compliance

PCI-DSS is a security standard for eCommerce companies to maintain a secure environment for credit card information. Compliance with the standards sets a baseline level of protection for customer data and helps reduce data breaches and fraud across the payment ecosystem.

It involves three main components:

Handling the credit card data of customers, ensuring they are securely collected and transmitted

Safely storing the data through 12 security domains of PCI standards, such as security testing, encryption, and monitoring

Annually validating that the required security controls are in place

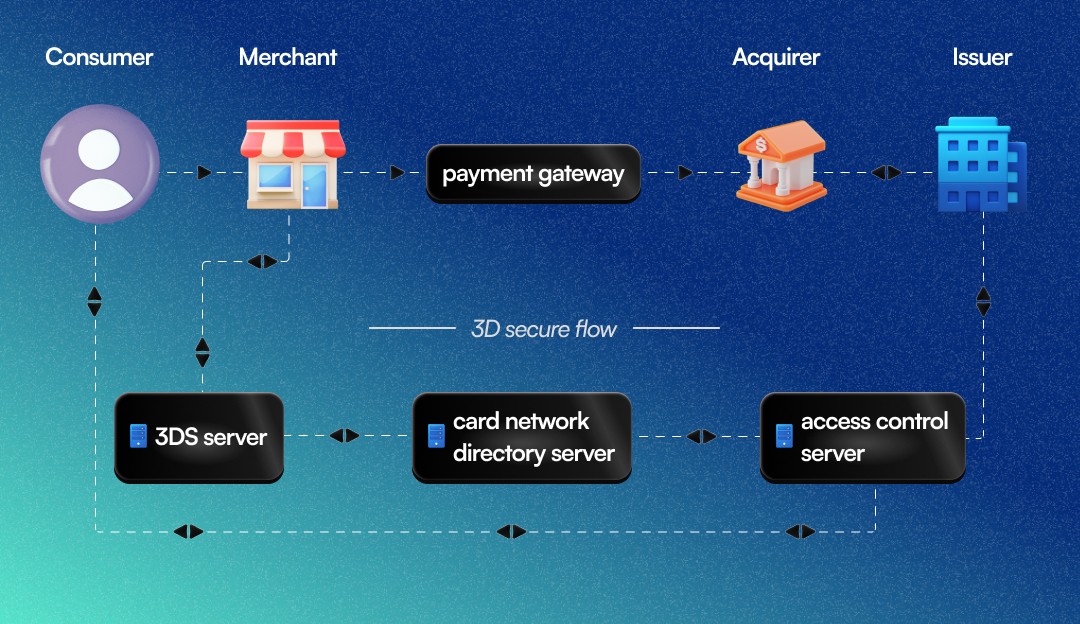

Implement 3D Secure protocol

A 3D secure protocol is also known as 3DS or payer authentication. It is designed to reduce the risk of fraud, theft, and other illicit activities during transactions.

The 3DS is an additional layer of authentication for online credit or debit card transactions. It asks customers to verify their identity with the card issuer during payment.

Customers are directed to a bank verification page, where they must type their password linked to the card or provide a code sent to their email or phone to verify their identity.

The image demonstrates the 3DS authentication process for verifying customer identity during online payments.

3D Secure Protocol

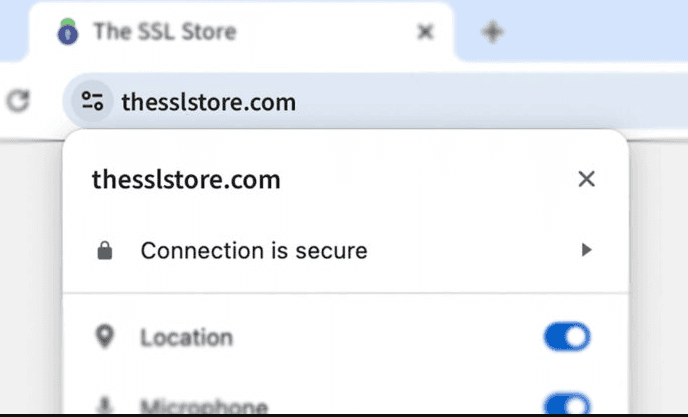

Use TLS for data encryption

TLS (Transport Layer Security) encrypts communication between web applications and servers. It ensures that information transmitted between customers and merchants is confidential and protected.

It encrypts the data being transferred from third parties

Ensures the parties are who they claim to be

Verifies the data for any tampering

It is the first defence against the loss of financial and personal information. The padlock icon on the web browser indicates that the TLS is enabled and the session is secure.

For example, the image shows a padlock sign in the address bar indicating the website has a secure HTTPS connection. This means the data transmitted between the user and the website is encrypted and protected.

Enable two-factor authentication (2FA)

2FA prevents unauthorised access and asks for other identification factors to verify the user. In addition to a password, it asks for OTP or mobile device verification.

It involves the following process:

The user logs in using their username and password

The server receives the credential and initiates the second verification

Two-factor authentication involves using any of the following authentication methods:

Hardware tokens, given by businesses to their employees

SMS verification, where the user is either asked to interact with the text message or provide the OTP sent through the SMS

Push notifications where a signal is sent to a mobile phone to approve/deny access

Voice-based authentication, where the automated voice asks the user to press a key or state their name

Biometrics information stored on mobile or laptop touchpads

Select the right payment gateway

A payment gateway works as the bridge between your eCommerce store and the customers. It integrates with your online store and enables you to accept customer payments through multiple payment methods.

Payment gateways access customers' sensitive financial data while processing a transaction. Therefore, ensuring your payment gateway is 100% secure makes sense.

Before investing in a payment gateway for your eCommerce store, ensure that you have answers to the following questions:

Is the payment gateway PCI DSS compliant?

What encryption methods are used to protect sensitive data?

Does the gateway offer fraud detection and prevention tools?

Are there security features like address verification and CVV checks?

How does the gateway handle data breaches, and what is its incident response plan?

Does the gateway offer tokenisation to protect customer payment information?

What authentication methods are used (e.g. 3D Secure)?

How often are security audits and penetration testing conducted?

What physical and network security measures are in place at their data centres?

How is customer data stored, and who has access to it?

What is the gateway's uptime guarantee and disaster recovery plan?

Are there options for additional security, like IP filtering or custom fraud rules?

Online payment gateways like Nimbbl provide the utmost importance to security. Nimbbl APIs follow all industry-standard security best practices and are PCI DSS compliant.

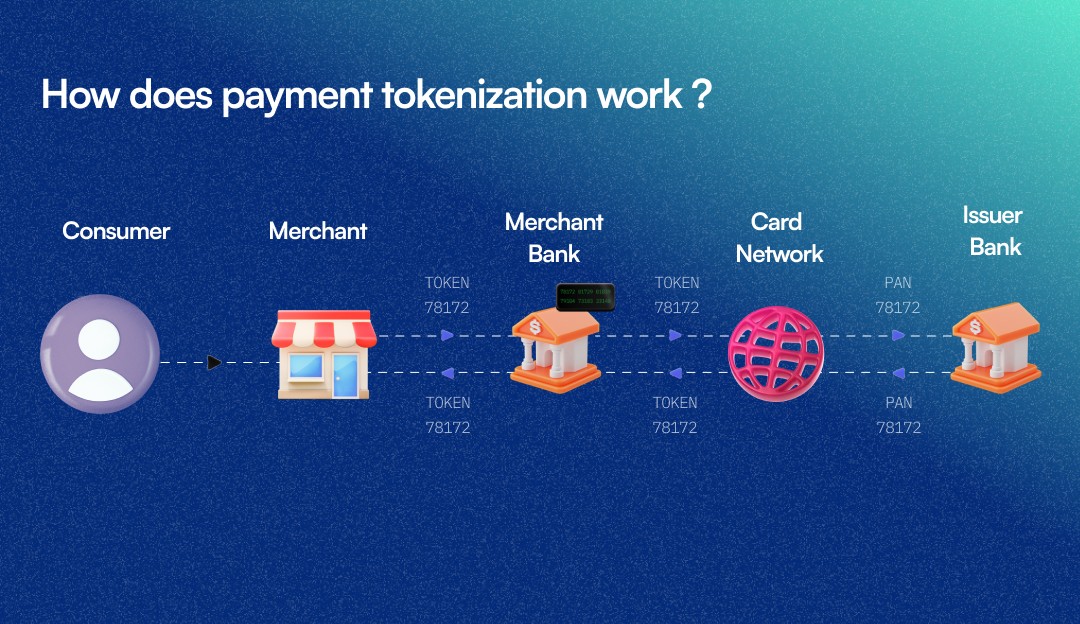

Opt for payment tokenisation

Tokenisation converts sensitive information into a unique identifier that cannot be used for any other transaction.

It is a unique string of numbers issued in real time that acts as a surrogate for the PAN(Primary Account Number). Hackers find it challenging to breach the code and exploit these tokens.

How does tokenisation typically work for online businesses and eCommerce stores?

A customer initiates making a transaction by entering card details

The merchant’s payment gateway sends a request to the PCI-compliant service provider, which creates a token for customer details

The payment service provider returns the token reference to the merchant and stores the mapping of the token to credentials

The payment gateway uses the token to request authorisation of payment instead of the original card data

The bank authorises the payment through token and notifies the merchant of the completed payment

The merchant then can store the token for future transactions

How does tokenisation work?

Use fraud detection tools

These tools use rule-based systems, advanced algorithms, and ML to identify and prevent fraud. They help analyse transaction patterns, flag suspicious activities, and block them.

There are three pillars of fraud protection and detection:

Rule engine: This uses predefined criteria to flag fraudulent transactions. It allows fraud analysts to quickly respond to new threats by adjusting the rules. For example, if it detects an attack on a specific IP address, the rule engine can block transactions from that address.

Machine learning: ML quickly analyses vast data of past transactions to identify patterns and anomalies indicative of fraud. It also identifies suspicious purchasing behaviour in real time, including sudden spikes in high-value transactions and unusual purchases. These systems enable prompt detection and fraud prevention, which makes them indispensable.

Link analysis involves mapping relationships between data points, such as transaction histories, customer accounts, shipping addresses, etc. Link analysis helps identify fraudulent networks to anticipate and prevent future fraud.

Communicate best practices with customers

Educating customers about secure online payment practices safeguards them against online payment fraud. Promote these measures and inform your clients of any new practices implemented.

For instance, Eventbrite addresses concerns like unknown charges on cards through FAQ.

Similarly, Zappos addresses security concerns through an FAQ page.

Conclusion

Securing online payments is critical today because of digital development, where cyber threats evolve continuously. Implementing these measures protects your business and valued customers from financial fraud.

With an online payment gateway like Nimbbl, you can effectively mitigate cyber threats and attacks and build a reputation for reliability.

Want to explore more?

Get in Touch

FAQs

What is security in online payment?

Security in online payment refers to implementing protocols to protect online transactions from unauthorised access, data breaches, and fraud.

How to make online payments more secure?

To secure online payments, consider implementing security measures like 2FA, 3DS, data encryption, etc. Use secure payment gateways, and regularly update your software for security patches.

How to secure online transactions?

Enabling encryption like TLS and adopting authentication methods like OTP or biometrics can ensure a secure online transaction. ML and AI monitoring systems can also be deployed to proactively detect suspicious activities.

How safe is online payment?

Online payment safety depends on security measures implemented by merchants and payment service providers. Proper security protocols can safeguard online payments against fraud.

Is there any risk in online payment?

If proper security measures are not implemented, online payments are at risk of phishing attacks, fraudulent transactions, data breaches, etc. Implementing robust security practices to mitigate online payment security threats is essential.