Suppose you are either a new eCommerce merchant about to launch your store or an experienced eCommerce store owner struggling to manage offline payment modes like cash on delivery (COD) and looking to replace them with different electronic payment systems. In that case, this is the article for you.

COD is 35% more expensive for sellers, especially during product returns. COD complicates the supply chain process by adding a new layer of transactions and increases cash collection cycles by over two weeks. In situations of product returns, the settlement periods are even longer.

This is primarily why popular eCommerce stores like Flipkart either shut down COD for specific locations or charge buyers an excess handling fee of INR 5 for each COD order.

Whether new or experienced eCommerce store, encourage customers to pay digitally. With a 42% increase in global cashless payments and the availability of fast payment options like – UPI, digital wallets, and payment gateways, it is the perfect time for Indian merchants to switch to different electronic payment systems.

This article will explain all the major types of electronic payment systems and their pros and cons.

Content Index

- What is an electronic payment system?

- What are the types of electronic payment systems?

- How to choose the best electronic payment system for your eCommerce store?

- Conclusion

What is an electronic payment system?

An electronic payment system is a digital platform that allows individuals and businesses to transfer funds securely. Examples include UPI, credit/debit cards, and digital wallets.

Electronic payment systems use encryption and security protocols for confidential financial transactions. Electronic payment systems are like modern-day couriers that securely transport money from one place to another. Just as you would use a trusted courier service to send valuable packages, electronic payment systems provide a reliable and secure way to transfer funds between individuals, businesses, and financial institutions.

India is experiencing a surge in digital transactions., with electronic payment systems taking center stage. In the last financial year, the value of digital payment transactions increased by 58%.

What are the types of electronic payment systems?

Below are the different types of electronic payment systems most popularly used in India:

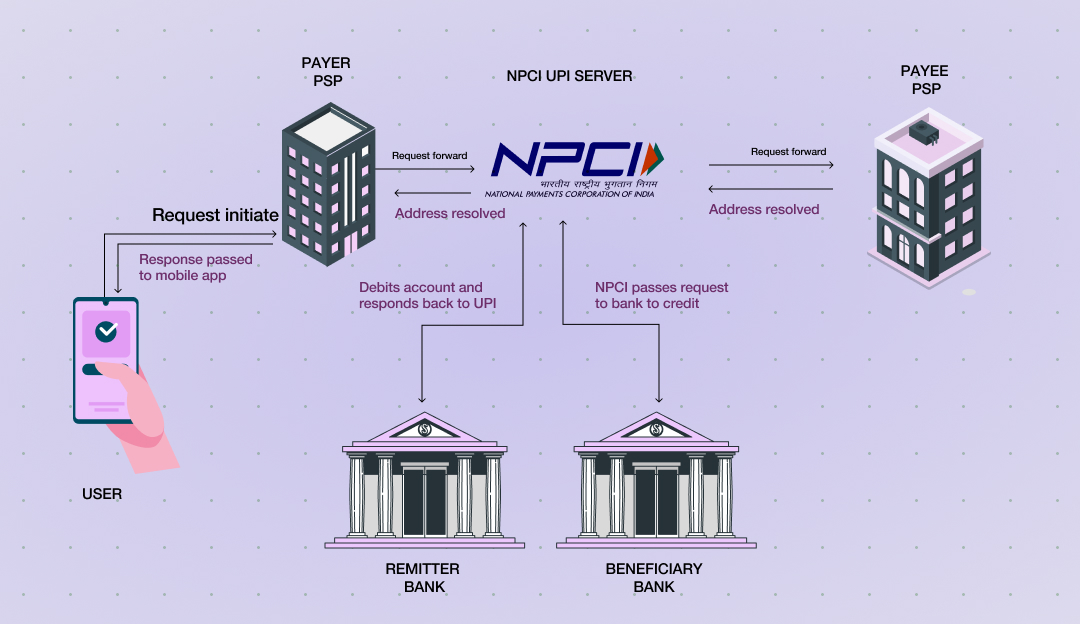

UPI

The full form of UPI is Unified Payment Interface, and until February 2023, it accounted for 75% of the overall transaction volume of India’s retail digital payment ecosystem. That means one in three retail transactions in India happens through UPI.

But what is UPI?

UPI allows users to transfer money from one bank account to another or different contacts through a mobile application. UPI is like a universal remote control for your bank accounts. Instead of juggling multiple remotes (bank apps/details) to access different accounts, UPI is a single interface that allows you to easily manage and transfer funds across all your linked bank accounts.

This single-window mobile payment system allows users to connect multiple bank accounts to the unified payment interface application and create specific virtual IDs for each account, known as UPI IDs.

- When sending money to another user/bank account, you need to select the bank from which you wish the amount to be debited, enter your unique PIN, and get confirmation of payment success

- While receiving money, you need to share your UPI ID with the sender, and they will follow the same process mentioned above to complete the transaction

Here’s how UPI works 👇

| Pros of UPI | Cons of UPI |

| UPI simplifies customer payment processing by eliminating the requirement of providing bank details for each digital transaction. This means improved customer satisfaction and greater possibilities of repeat purchase UPI is easy to integrate within your online store, highly secured with 2FA and biometric verification, and has a much lower transaction fee compared to traditional payment systems | UPI’s accessibility is dependent on smartphones. Hence, if a customer is shopping from any other device, the effectiveness of UPI as a payment option may be limited. |

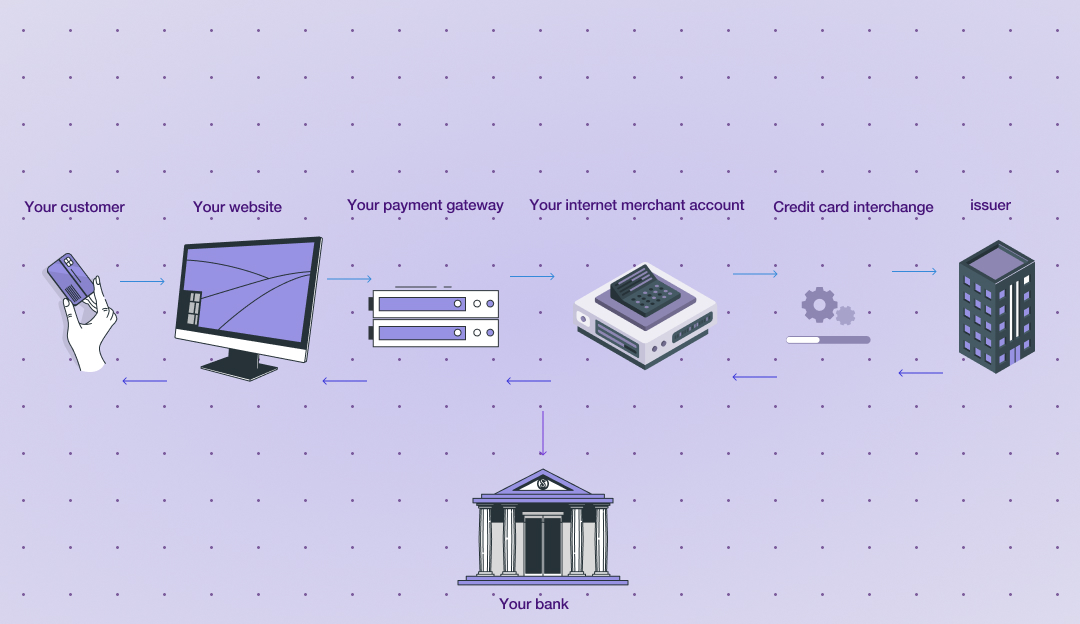

Credit Cards

Credit cards are India’s go-to payment system for online and offline transactions. As an electronic payment system, it provides a line of credit up to a pre-defined limit.

They’re similar to borrowing money from a friend, but the bank lends you funds up to a specific limit instead of your friend. You can make purchases now and repay the bank later, with the added benefit of building a credit history.

Users receive a monthly statement listing all credit card transactions and the outstanding balance that needs to be paid. Credit cards continued to grow in FY 2023-2024, with their overall transaction volume reaching 0.79 billion in India.

Credit cards offer the convenience of purchasing a desired item instantly, without worrying about cash leaving your bank right away, and that’s what tempts many users.

Here’s how a credit card works 👇

| Pros of credit card | Cons of credit card |

| Credit Cards are universal payment modes. A credit card empowers your customers to make payments in multiple currencies. This improves the possibilities of completing a checkout in case of international transactions Credit Card payments improve business cash flow by speeding up the payment process. That means predictable cash inflow and reduced payment cycles Credit risk is not passed to the merchant with credit cards. The standardisation of protocols for settlement and disputes makes it easier for merchants to manage customer experience investments better. | The transaction fees associated with Credit Cards can be huge. High-frequency or high-value transactions can affect both business owners and customer A credit card can add to a longer checkout process for an online purchase, as the data entries to be made can be huge. |

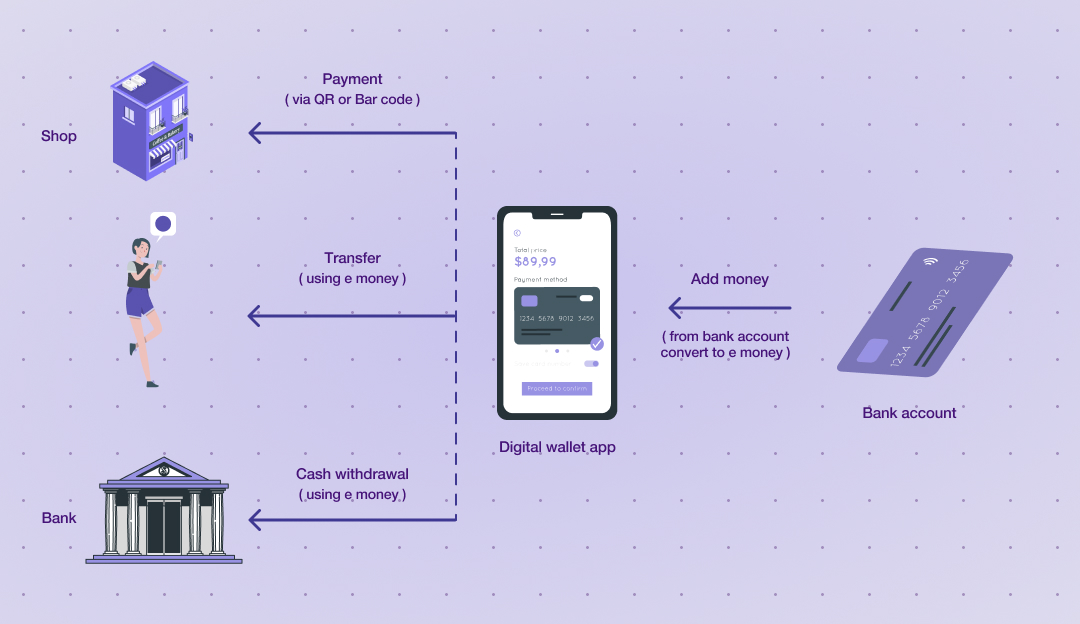

Digital Wallets

The next name in our list of electronic payment systems is digital wallets. Digital wallets securely store payment information like bank details, credit/debit card information, and e-vouchers. That way, you don’t need to carry your credit card every time or add credit card details during each online transaction. You can use your digital wallet balance to complete transactions.

Here’s how digital wallets work👇

| Pros of digital wallet | Cons of digital wallet |

| Digital wallets are secured with biometric authentication and offer the convenience of not carrying physical cash to your end users. This increases the possibility of repeat purchase Digital wallets are great for customer retention. Merchants can easily integrate them with loyalty programs and promotions to increase overall loyal customers and encourage repeat purchases | Digital wallets are vulnerable to technology issues and network failures and require regular software updates. All these can affect the buying experience, resulting in more abandoned carts |

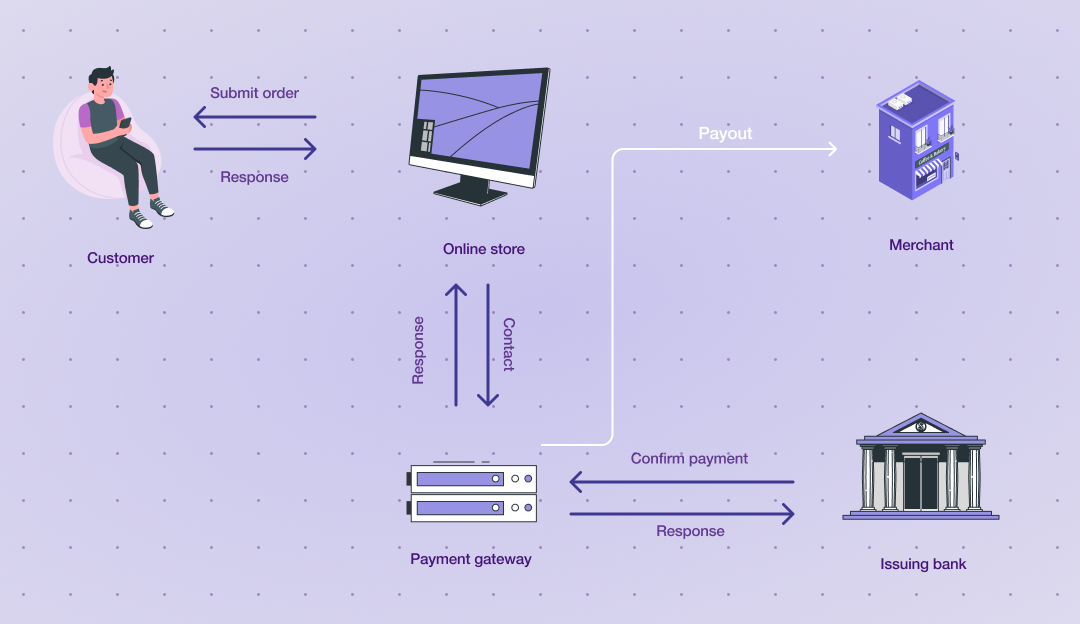

Payment Gateways

A payment gateway bridges the gap between customers and financial institutions. It helps businesses smoothly collect customer payments through their websites or mobile applications without compromising customers’ experience.

A payment gateway is an electronic payment system that processes transactions in real-time with complete data protection. It seamlessly enables safe money flow from a customer’s bank account to a merchant’s account.

Here’s how a payment gateway works 👇

| Pros of payment gateways | Cons of payment gateways |

| Payment gateways optimize a shopper’s checkout experience by fetching the payment options for which they are eligible. By simply inserting their contact number, users can get an overview of the best payment options available without the trouble of toggling between applications to get OTPs or remember their UPI IDs. This is an excellent way for an eCommerce merchant to convert more browsers into buyers and increase repeat purchases. | Sometimes, payment gateways are difficult to integrate within your eCommerce platform, and you may require additional steps and technical help. But if you go for a no-code payment gateway, you can easily avoid these challenges. |

Pros and Cons of Payment Gateways

How to choose the best electronic payment system for your eCommerce store?

Before selecting an electronic payment system for your business, consider focusing on the following factors:

Customer’s preference and convenience

First, your customers must be aligned with your selected electronic payment system. For example, if your target customers are Millennials and GenZs, providing all the modern payment systems like UPI, payment gateways, digital wallets, and credit cards makes sense. This is especially true because GenZ and millennials are three times more likely to use an alternative payment method to cash, like contactless payment apps or buy now pay later.

ECommerce merchants aim to develop a convenient digital journey where the experience from browsing to buying is a no-brainer. That’s precisely why we prioritise customers’ preferences when choosing types of electronic payment systems.

Level of security and data protection

Customers trust you big time When they insert their credit card details, PIN, contact number, and other sensitive information online! Therefore, select an electronic payment system that complies with all the Reserve Bank of India (RBI) regulations, such as the Payment and Settlement Systems Act, 2007, Guidelines on Prepaid Payment Instruments (PPIs), etc.

Additionally, it enables two-factor authentication and end-to-end encryption to prevent fraud attempts at data breaches.

Transaction fees

Different payment systems charge different types based on various factors, such as frequency of payment, currency, domestic or international transactions, etc. Before selecting one, merchants must weigh these transaction fees against the respective payment system, customers’ convenience, and potential benefits.

For example, credit card merchants who receive payments from customers via digital wallets on UPI must pay an interchange fee of 1.1% for transactions exceeding Rs. 2000. But, the transaction is free for customers, and UPI is enormously convenient. Therefore, providing UPI as an e-payment option is a good idea despite the interchange.

Compatibility with your eCommerce platform

Whatever eCommerce platform you use—Shopify, BigCommerce, Wix, or any other—ensure the electronic payment system is compatible. Suppose it takes forever to integrate the payment system with your eCommerce platform, or there are frequent collapses due to poor compatibility. In that case, it will only affect customers’ experience, and that’s the last thing you want!

Conclusion

The speed at which electronic payment systems spread across the Indian eCommerce market is next-level. Most of these systems are carefully designed to meet common merchant frustrations, such as extended payment cycles, complex integrations, and customer inconvenience!

Pick your electronic payment system wisely, weigh the pros and cons, and finally decide.

If you are looking for a payment gateway that offers customers a one-click checkout without a long integration process, try Nimbbl.

Nimbbl helps you with:

- Managing payment operations with one integration

- Offer your customers with new-age payment options like BNPL

- Simplifies checkout experience with one-click checkout

Want to give it a try?