Online stores need to keep up with the ever-changing payment ecosystem. No matter how personalized your shopping experience is, if you still offer the same old payment options like net banking and cash on delivery, you leave money on the table.

The youth of India are more comfortable with new-age payment methods, and one of those emerging payment methods is Buy Now Pay Later or BNPL.

Growing at a CAGR of ~321 % by Gross merchandise value during FY’19-FY’21, BNPL provides a more convenient way for customers to buy from you.

These apps let customers pay for their purchases in smaller instalments or in full at a later, specified time. This translates to lower abandonment rates, bigger checkouts, and a better customer experience. Plus, BNPL options open your store’s doors to a broader range of shoppers with different budgets.

If you are confused between multiple BNPL apps in India, we’ve got your back. This article discusses what a BNPL platform is and how it works.

Content Index

- What is a Buy Now Pay Later App and How Does It Help?

- How Does a Buy Now Pay Later App Work?

- Current Scenario of BNPL Apps In India: Are They Succesful?

- 2 Reliable Buy Now Pay Later Apps in India in 2024

- How do you select a BNPL App in India?

- Why Stick to a Single BNPL app When You Can Have It All?

What is a Buy Now Pay Later App and How Does It Help?

Buy Now Pay Later apps are payment platforms that allow users to buy without requiring them to pay the total amount upfront. These platforms allow customers to spread payments over time or pay the total amount on a pre-decided later date.

This flexibility to ‘delay payments’ “influences consumers to perceive purchases as less expensive,” Rhys Aby writes in a study. He also comments that BNPL transactions lower the ‘pain of payment’ and lead to customers spending more.

If you are curious to know about more benefits you reap by choosing BNPL options for your eCommerce store, here’s a breakdown of some of them:

Increase in the number and value of purchases

Customers who spread out payments are more willing to buy bigger-ticket items. They’re also prone to buy more frequently because of this convenience and the psychological comfort of paying later.

Ability to reach more customers

Multiple payment methods attract more customers, especially younger folks who might not have/want to opt for a traditional credit card. This is because young, salaried customers only sometimes have a constant flow of income to meet their daily expenditures.

Many might also be unable to apply for credit cards, as those require deeper credit checks and significant documentation. Most credit cards also charge an annual fee and comparatively higher interest rates, something customers don’t have to bear with this mode of payment.

Guaranteed payments

BNPL services absorb risk as you receive guaranteed payments for all successful transactions. Whether the end customer ultimately pays or not is not something for you to worry about. You are also protected against payment or consumer fraud.

How Does a Buy Now Pay Later App Work?

A BNPL app works a lot like other payment methods except that it does not require customers to make immediate payments for their purchases. Here’s a breakdown of the steps:

- The merchant integrates a BNPL app, which appears to the customer as one of the many modes of payment when checking out

- Once the customer selects a BNPL payment platform, they are required to sign up to the app for a basic KYC that requires them to fill in details like name, address, age, and a government ID proof

- Unlike a credit card that requires substantial evidence of credit history and more paperwork, BNPL apps have less strict eligibility criteria for quick credit

- When checking out, customers agree to pay the purchase amount at a later period, viz. after a fortnight or a month or as EMIs

- Once the purchase is made, the customer must pay the amount at the designated period to avoid a fine

📒FYI: The merchant flow will differ if you are pre-approved with a direct download and onboarding through the BNPL app. It will be something like this:

While everyone uses BNPL for their convenience and freedom, these services exclusively appeal to customers:

- Desirous of making large purchases but not willing to shell large amounts in one go

- Salaried employees with low savings who cannot wait to push a purchase until payday

- People in Tier-2 and Tier-3 cities with lower savings and average earnings

- Those looking for EMI options

Current Scenario of BNPL Apps In India: Are They Succesful?

While BNPL apps are still very much in demand within India, their operational procedure often raises questions about how safe they are for eCommerce merchants and their customers. The Reserve Bank of India has imposed strict regulations to protect unsecured personal loans, especially in BNPL. According to this Forbes article, Measures include hiking the minimum capital banks and NBFCs need to hold against loans and curtailing non-bank lending through prepaid cards and digital wallets.

This has forced many BNPL apps like ZestMoney to shut down their operations, while Paytm and Slice are pivoting their business models with a focus on high-value loans with lesser credit risks. These apps have also made it a point to evaluate a customer’s creditworthiness before granting a loan.

Though BNPL is still a critical pillar in the Indian online payment ecosystem, it requires more guardrails. While this is leading many BNPL apps towards failure, it also ensures a safer finance ecosystem for India.

2 Reliable Buy Now Pay Later Apps in India in 2024

If you want to integrate a BNPL app into your eCommerce store, here are the two most trusted BNPL apps for Indian customers:

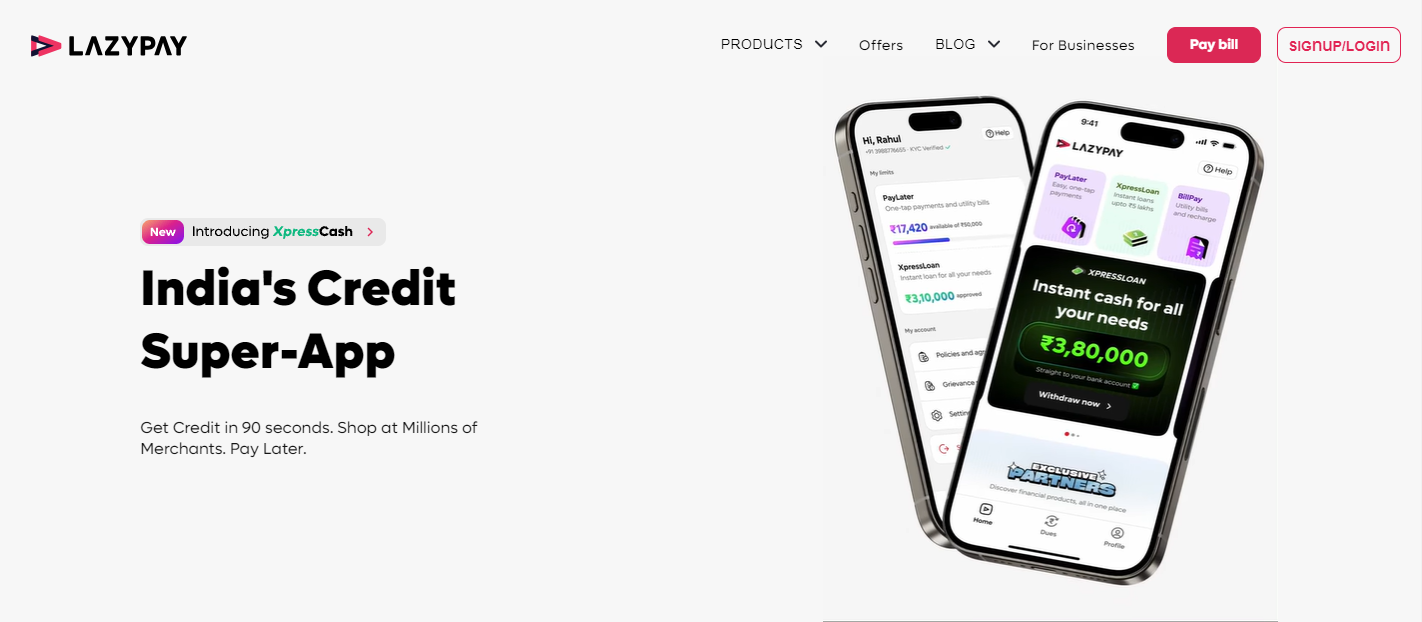

LazyPay

LazyPay is a leading BNPL platform backed by global fintech giant PayU Finance. It offers a hassle-free BNPL service with a ‘One-tap checkout’ feature that lets customers pay without entering OTPs or PINs. It is available for all salaried Indian citizens between 22 and 55 years old. To avail of LazyPay’s BNPL service, customers only need their PAN, Aadhaar, and a photograph to get a credit limit of up to Rs. 5 lakh.

Key Benefits

- 15-Day Interest-Free Period: Lets customers stock up on goodies and pay it all back within 15 days at no extra charges

- Pay-in-Parts Option: Choose a 3, 6, 9, or 12-month instalment plan, some with zero interest

- Instant Personal Loans: Allows for a quick personal loan of up to 5 lakh rupees with LazyPay’s XpressLoan

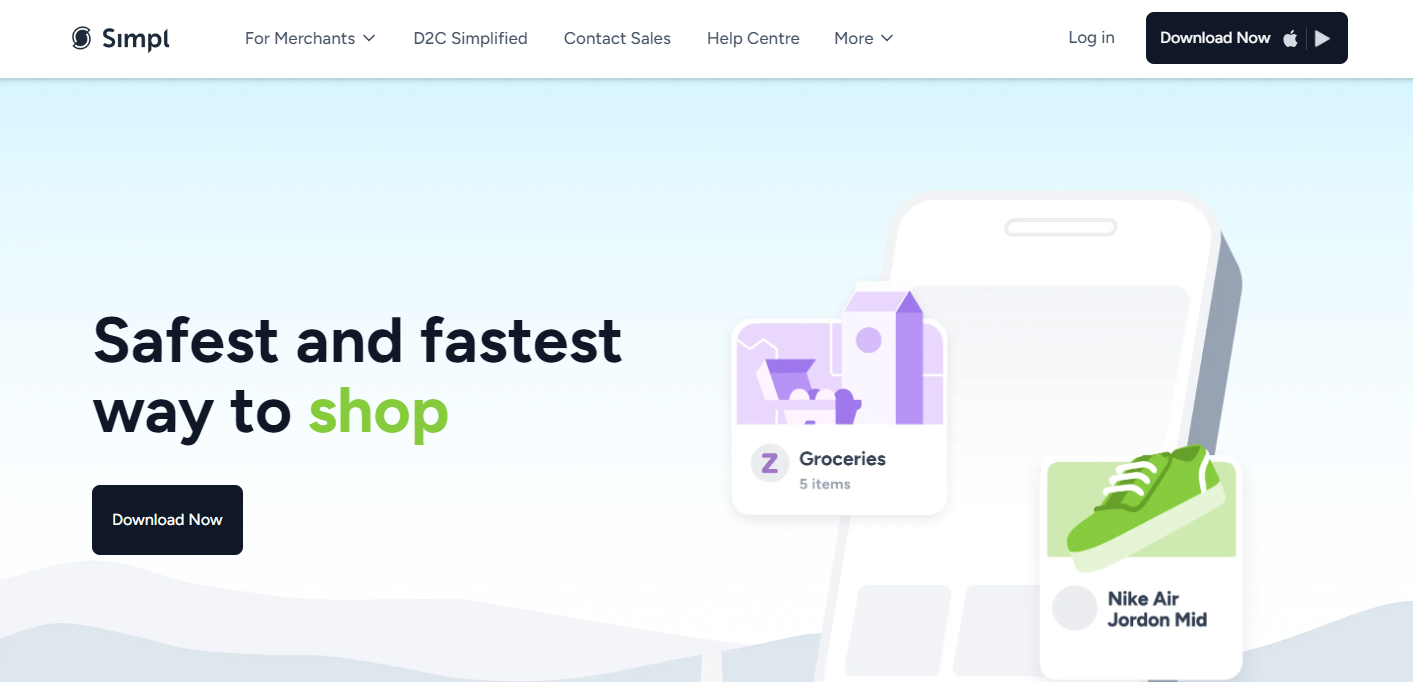

Simpl

With a user-friendly app and instant credit approvals, Simpl empowers customers to purchase with one tap, eliminating the need for lengthy forms or credit card approvals. Customers pay back every 15 days, on the 5th or 20th of the month. It also allows customers to split larger purchases into three interest-free payments.

Key Benefits

- Flexible Timeline: Pay the first part at checkout and the rest within 2 months through the app

- Quick Integration: Easy integration ensures you get Simpl up and running on your online store in just 2 minutes

- Buyer Protection: Give your customers peace of mind knowing their purchases are protected with cutting-edge security

- Instant Payouts: Get paid upfront while your customers enjoy flexible payment options

How do you select a BNPL App in India?

Choose a BNPL app that fits with your business

Not all Buy Now Pay Later providers are the same. Some are suited for more significant bulk transactions, while others are more customer-oriented with more payment options. You should also consider whether the provider you choose can handle the average number of transactions on your eCommerce store and whether it can integrate easily with your existing tech stack.

If your eCommerce site attracts most of its mobile traffic, check whether the BNPL provider is natively compatible with iOS and Android interfaces. Most importantly, ensure the BNPL service integrates with your eCommerce platform without hiccups.

Ensure the service provides plenty of flexibility for customers

You’re adding a BNPL option in your eCommerce store to give customers more choices regarding how they want to pay. Ideally, a BNPL service should offer multiple options without complicating the checkout experience.

Check all the providers’ payment terms and review the instalment lengths, frequency, and interest rates. Plus, there should be the option for the customer to pay the remaining instalments at once

Ensure that the BNPL app covers all the major payment providers and is geographically compatible with all the regions where you get the most traffic.

Verify the security of your platform of choice

Strong security measures are non-negotiable with anything payment-related. Ensure your BNPL provider has robust user identification and credential management features.

Check if the provider has a firm password policy. Opt for platforms with Multi-factor Authentication (MFA) support. Options for encrypted biometric scanning are a bonus.

Lastly, the terms and conditions and privacy policy must be reviewed to ensure sensitive data remains safe from prying hands. Encryption keys should have proper rotation policies, and regular auditing processes should be in place.

Why Stick to a Single BNPL app When You Can Have It All?

You can integrate with any of these BNPL apps or choose a single, intelligent checkout solution that integrates with all of them.

Introducing Nimbbl one-click checkout.

With a simple integration, you’ll get access to all the top BNPL apps in India in one place through our API. This means Nimbbl’s intelligent payment router will connect your customers with the BNPL app of their choice to optimize their payment experience.

Want to know more?